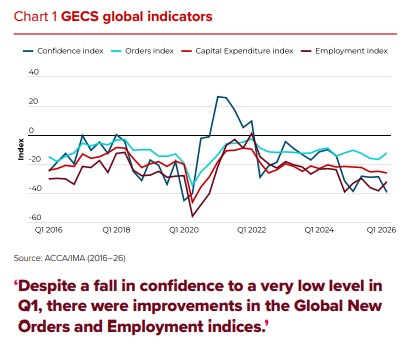

The ACCA-IMA Q1 2026 Global Economic Conditions Survey (GECS), released on 21 April 2026, reveals a stark reality for the Malaysian economy. Business confidence among finance professionals has plummeted to levels not seen since the 2020 pandemic lockdowns.

Conducted between 3 and 19 March, coinciding with the escalation of conflict in the Middle East, the survey paints a picture of a nation at the intersection of a “polycrisis“: high energy costs, supply chain fragility, and a volatile Ringgit.

THE “SOBERING” DATA: A Pandemic-Era Replay?

The GECS report indicates that Malaysia is grappling with its fourth major global shock of the decade. Unlike the purely biological shock of 2020, the 2026 crisis is “deeply geopolitical.”

- Confidence Collapse: Sentiment among CFOs and finance leaders has fallen sharply, nearing historic lows.

- The 33% Factor: While 25% of global respondents cited geopolitics as their top risk, that number surged to 33% in the Asia-Pacific region.

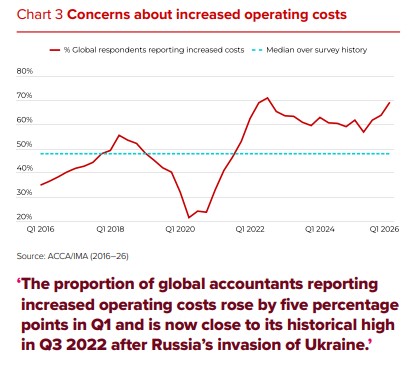

- Operating Costs: Reports of rising operating costs are at their highest since Q3 2022, driven by the $100 oil barrier and disrupted maritime routes.

MALAYSIA’S STRATEGIC VULNERABILITIES

As a critical node in the global electronics and energy markets, Malaysia is uniquely exposed to the Middle East fallout.

| Impact Driver | Economic Consequence | Sector Most At Risk |

| Energy Import Costs | Higher oil/gas prices increase the national subsidy burden and industrial overheads. | Logistics & Manufacturing |

| Semiconductor Hub | Disruptions in petrochemical inputs and critical materials lead to production delays. | Electrical & Electronics (E&E) |

| US Dollar Strength | A “Flight to Safety” strengthens the USD, placing immense downward pressure on the MYR. | Import-Dependent Retail & SMEs |

| Cybersecurity | Ranked as the #2 global risk (17%); critical for Malaysia’s digital finance ambitions. | Fintech & Banking |

THE SILVER LININGS: Structural Resilience

Despite the “sobering” sentiment, two indicators suggest Malaysia’s underlying economic engine has not yet stalled:

- The Global New Orders Index: This has returned to its historical average, indicating that global demand for Malaysian exports remains robust.

- The Employment Index: Hiring intentions showed a slight improvement, suggesting that firms are holding onto talent in anticipation of a “post-conflict” recovery.

Editor’s Take: The “Intelligence Premium”

Q1 GECS findings reveal a paradox: orders are coming in, but the “fear factor” is at an all-time high. This suggests we are in an “Intelligence-Driven Market.” The businesses that survive the 2026 “squeeze” won’t be those with the lowest costs, but those with the best Geopolitical Risk Intelligence.

As Andrew Lim noted, the two are now inseparable. For Malaysia, the goal is to protect the RM18 billion in FDI flowing into the JS-SEZ and the RM68 billion Halal export engine from being derailed by currency volatility and maritime bottlenecks. Finance professionals must stop looking at the balance sheet in isolation and start looking at the map.