The ongoing crisis in West Asia has evolved from a localized geopolitical flashpoint into a slow-moving, long-lasting macro shock that is actively reshaping global labor markets.

According to a definitive policy update released by the International Labour Organization (ILO), titled “Employment and Social Trends May 2026 Update: Growing labour market risks of the Middle East crisis,” rising energy overheads, maritime transport disruptions, and fracturing migration pipelines are triggering an extensive degradation of working conditions, incomes, and jobs worldwide.

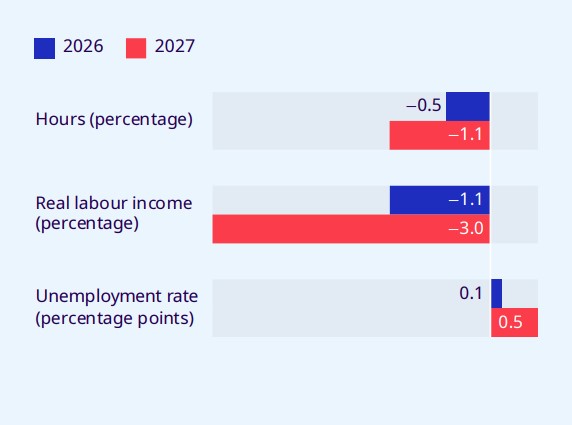

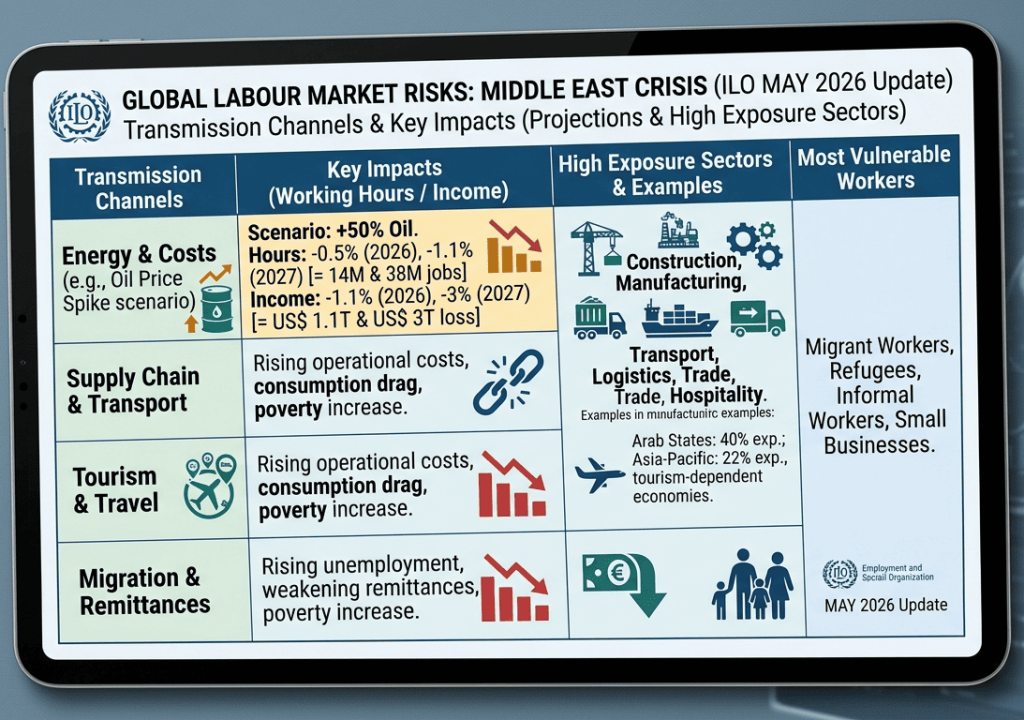

The baseline econometric modeling from the report presents a sobering narrative for emerging markets. Under an illustrative scenario where global oil prices spike 50% above their early 2026 average, the shockwaves passing through corporate balance sheets will contract global working hours by 0.5% in 2026 and 1.1% in 2027. Mechanically, this translates to the destruction of 14 million and 38 million full-time equivalent jobs, respectively.

The Macro Transmission Channels: From Cost Shocks to Income Cuts

The research, authored by ILO Chief Economist Sangheon Lee, highlights that the world of work is the primary conduit through which external geopolitical friction mutates into personal financial distress. As operating margins contract under the weight of an unexpected US$3 trillion global labor income wipeout by 2027, the structural adjustment is falling heavily on high-exposure sectors.

1. The Arab States Vulnerability

As the epicenter of the crisis, the Arab States face a devastating economic contraction. Under a severe escalation scenario, total working hours in the region are projected to plumet by 10.2% – a collapse more than double the scale recorded during the peak of the COVID-19 pandemic in 2020. With 40% of regional employment tied to construction, manufacturing, transport, and trade, the internal labor market is facing a systemic unwinding.

2. The Asia-Pacific Vulnerability

Due to its intense integration with Gulf energy flows and legacy labor corridors, the Asia-Pacific region is highly exposed. The ILO projects an aggregate decline of 1.5% in working hours and a severe 4.3% drop in real labor incomes by 2027. Roughly 22% of the region’s workforce sits directly within high-exposure sectors, with tourism-reliant and energy-import-dependent economies bearing the immediate brunt of the slowdown.

The Remittance Lifecycle: A Lifeline Under Strain

A critical area of concern highlighted by the ILO is the sudden fracturing of cross-border migration corridors. Historically a reliable economic cushion for South and Southeast Asian economies, labor deployments to the Gulf Cooperation Council (GCC) bloc have fallen sharply.

Flight cancellations, localized security threats, and a defensive pull-back in GCC construction and hospitality projects have slowed new labor deployments while accelerating migrant repatriations. The resulting contraction in remittance flows creates a highly dangerous downstream effect of weakening local household consumption, worsening poverty indices, and placing severe counter-pressures on the domestic labor markets of the home nations.

Editor’s Take: Managing the ‘Human Bill’ of Global Supply Friction

For the Malaysian Business reader, the ILO’s sobering print provides a critical frame of reference for navigating the domestic market. On the surface, Malaysia’s economic indicators appear insulated: our corporate landscape is cushioned by a RM426.7 billion national investment pipeline, and institutions like MBSB Bank have moved swiftly to roll out RM5 billion in SME Stabilisation Relief Funds to shield local trade lines.

However, corporate captains must realize that financial liquidity programs are merely short-term shock absorbers; they cannot permanently defer the “Complexity Tax” of a prolonged geopolitical crisis.

When global labor income contracts by US$3 trillion, global demand follows it down. For an export-driven nation, this is where external friction shifts into a local reality. As energy and shipping overheads climb, the temptation for corporate boards to manage margins by cutting working hours or freezing recruitment will intensify.

The ILO report accurately identifies this as a dangerous pivot that threatens to turn a temporary energy shock into a structural crisis for decent, secure work.

To avoid this trap, our corporate and state leadership must focus on Productivity Realism and architectural simplicity. Rather than treating labor purely as an elastic variable to be squeezed during down-cycles, enterprises must use this period of volatility to accelerate digital automation and upskilling frameworks—mirroring the structural efficiencies seen in CelcomDigi’s recent Q1 margin expansions or Johor Plantations’ circular midstream pivots.

By building an agile, high-skilled operational base today, Malaysia’s enterprises can insulate their working conditions from external shocks, protecting our domestic capital velocity and ensuring our workforce emerges more resilient in a volatile, multipolar global economy.